As filed with the Securities and Exchange Commission on May 17, 2006.

REGISTRATION NO. 333-129199

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM SB-2/A-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

BMB MUNAI, INC.

---------------------------------------------

(Name of Small Business Issuer in its Charter)

Nevada 1311 30-0233726

- ------------------------------- ---------------------------- -------------------

(State or Other Jurisdiction of (Primary Standard Industrial (I.R.S. Employer

Incorporation or Organization) Classification Code Number) Identification No.)

202 Dostyk Ave. 4th Floor, Almaty Kazakhstan 050051

+7 (3272) 375-125

--------------------------------------------------------------------------

(Address and Telephone Number of Registrant's Principal Place of Business)

Gateway Enterprises, Inc.

3230 East Flamingo Road, Suite 156 Las Vegas, Nevada 89121

800 992-4333

--------------------------------------------------------

(Name, Address and Telephone Number of Agent for Service)

Copy to:

Ronald L. Poulton, Esq.

Poulton & Yordan

324 South 400 West, Suite 250, Salt Lake City, Utah 84101

(801) 355-1341

Approximate Date of Proposed Sale to the Public: From time to time after this

Registration Statement becomes effective.

If this Form is filed to register additional securities for an offering pursuant

to Rule 462(b) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective

registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under

the Securities Act, check the following box and list the Securities Act

registration statement number of the earlier effective registration statement

for the same offering. [ ]

If any of the securities being registered on this Form are to be offered on a

delayed or continuous basis pursuant to Rule 415 under the Securities Act of

1933 check the following box. [ ]

If delivery of the prospectus is expected pursuant to Rule 434, please check the

following box. [ ]

CALCULATION OF REGISTRATION FEE

Title of each Number of Proposed Maximum Proposed Maximum Amount of

Class of Securities Securities Offering Price Aggregate Offering Registration

to be Registered to be Registered Per Share(1) Price (1) Fee(2)

- -------------------------------------------------------------------------------------------------------------------------

Common Stock 13,846,427 $10.25 $141,925,877 $15,187

- -------------------------------------------------------------------------------------------------------------------------

(1) Estimated pursuant to Rule 457(c) solely for the purpose of calculating the

amount of the registration fee, using the average of the bid and asked

prices as reported on the Over-the-Counter Bulletin Board ("OTCBB") on May

12, 2006.

(2) $3,692 of this fee was paid with the initial filing of the Registration

Statement on Form SB-2, SEC File #333-129199 on October 24, 2005. The

remaining $11,495 was paid on or before May 12, 2006.

The Registrant hereby amends this registration statement on such date

or dates as may be necessary to delay its effective date until the registrant

shall file a further amendment which specifically states that this registration

statement shall thereafter become effective in accordance with Section 8(a) of

the Securities Act of 1933 or until this registration statement shall become

effective on such date as the Commission, acting pursuant to said Section 8(a)

may determine.

PROSPECTUS

13,846,427 Shares of Common Stock

[BMB Muani's Logo]

This prospectus relates solely to the offer and sale by the selling stockholders

identified in this prospectus of up to 13,846,427 shares of our common stock,

all of which are currently outstanding. The selling stockholders are offering

all of the shares to be sold in the offering, but they are not required to sell

any of these shares. We will not receive any of the proceeds from the sale of

our common stock by the selling stockholders. We will bear all expenses (other

than selling commissions and fees and expenses of counsel or other advisors to

the selling stockholders) relating to this offering.

The selling stockholders may sell these shares from time to time in various

types of transactions, including in the principal market on which the stock is

traded or listed or in privately negotiated transactions. If any broker-dealers

are used by the selling stockholders, any commissions paid to broker-dealers

and, if broker-dealers purchase any shares of our common stock as principals,

any profits received by such brokers-dealers on the resale of shares of our

common stock, may be deemed to be underwriting discounts or commissions under

the Securities Act of 1933. In addition, any profits realized by the selling

stockholders may be deemed to be underwriting commissions if any such selling

stockholder is deemed an "underwriter" as defined in the Securities Act of 1933,

as amended.

Our common stock is traded on the Over-the-Counter Bulletin Board under the

symbol "BMBM.OB." The average of the bid and ask price per share of our common

stock as reported by the Over-the-Counter Bulletin Board on May 12, 2006, was

$10.25

Investing in these Shares involves a high degree of risk. See "RISK FACTORS"

beginning on page 5 to read about factors you should consider before buying our

stock.

Neither the Securities and Exchange Commission nor any state securities

commission has approved or disapproved of these securities or passed upon the

accuracy or adequacy of this prospectus. Any representation to the contrary is a

criminal offense.

You should rely only on the information contained in this prospectus. Neither we

nor the selling stockholders have authorized anyone to provide you with

information different from that contained in this prospectus. The selling

stockholders are offering to sell, and seeking offers to buy, shares of our

common stock only in jurisdictions where offers and sales are permitted. The

information contained in this prospectus is accurate only as of the date of this

prospectus, regardless of the time of delivery of this prospectus or of any sale

of our common stock.

The date of this Prospectus is_________, 2006.

PROSPECTUS SUMMARY

Our Company

We are an independent oil and natural gas company engaged in the

acquisition, exploration, development and production of crude oil and natural

gas properties in the Republic of Kazakhstan, (sometimes also referred to herein

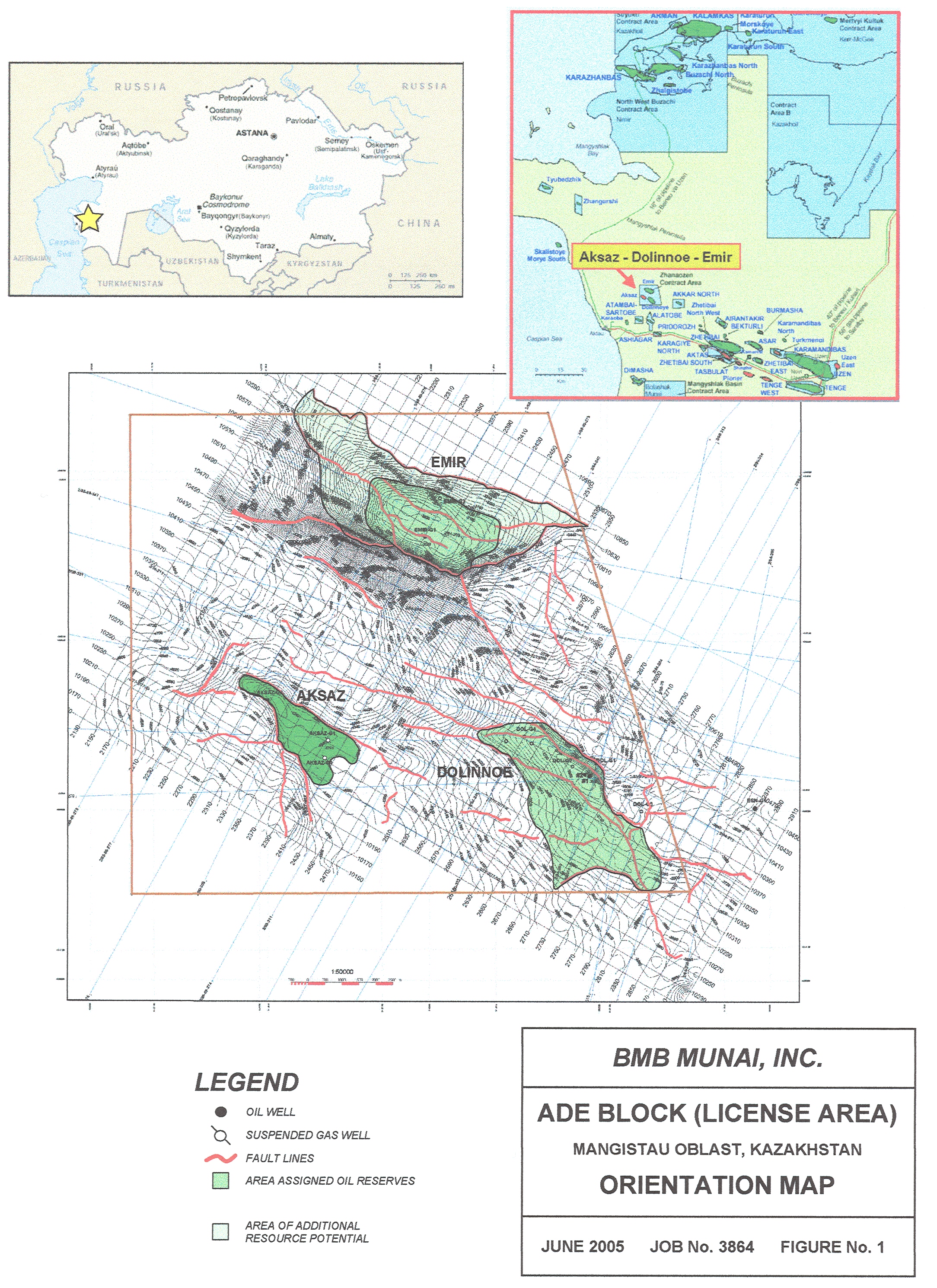

as "Kazakhstan" or the "ROK"). We hold a contract that allows us to explore and

develop approximately 460 square kilometers in western Kazakhstan. Our contract

grants us the right to explore and develop the Aksaz, Dolinnoe and Emir oil and

gas fields (the "ADE Block"), as well as an area adjacent to these fields which

we refer to as the Extended Territory.

We are currently in the development stage. We generate revenue, income

and cash flow by producing and marketing oil from test production from our oil

and natural gas properties. We make significant capital expenditures in our

exploration and development activities, which we anticipate will allow us to

increase and improve our ability to generate revenue. Our drilling strategy is

focused toward enhancing cash flows by drilling developmental wells within a

proximity of existing wells. Along with improving cash flows, we seek to

increase our reserves by drilling exploratory wells to find new reservoirs or

extend known reservoirs. We believe this strategy will result in growth of

proved developed reserves, production and financial strength.

Our principal executive offices are located at 202 Dostyk Ave., 4th

Floor, Almaty, Kazakhstan 050051. We also maintain a U.S. office in Salt Lake

City, Utah, located at 324 South 400 West, Suite 250, Salt Lake City, Utah

84101. Our telephone number in Almaty is +7 (3232) 375-125. Our telephone number

in Salt Lake City is (801) 355-2227. Our website address is www.bmbmunai.com.

Company Information

We originally incorporated in Utah in July 1981 under the name Au `n

Ag, Inc. The corporation later changed its domicile to Delaware in February

1994. In April 1994, the corporation changed its name to InterUnion Financial

Corporation ("InterUnion"). On November 26, 2003, InterUnion executed an

Agreement and Plan of Merger with BMB Holding, Inc., a private Delaware

corporation, formed for the purpose of acquiring and developing oil and gas

fields in the Republic of Kazakhstan. As a result of the merger, the

shareholders of BMB Holding, Inc., obtained control of the corporation. BMB

Holding, Inc., was treated as the acquiror for accounting purposes. A new board

of directors was elected that was comprised primarily of the former directors of

BMB Holding, Inc. In connection with the Agreement and Plan of Merger, the name

of the corporation was changed to BMB Munai, Inc. We changed domicile of the

corporation from Delaware to Nevada in December 2004.

The Offering

Securities Offered: 13,846,427 Shares of $0.001 par value

Company common stock.

Use of Proceeds: All of the net proceeds from the sale or our

common stock covered by this prospectus will

be received by the selling stockholders who

offer and sell shares of our common stock.

We will not receive any proceeds from the

sale of our common stock offered by the

selling stockholders.

OTC Bulletin Board Symbol: "BMBM.OB"

2

Summary Financial Information

The table below provides you historical summary financial data for the

fiscal year ended March 31, 2005 and the period from inception, (May 6, 2003)

through March 31, 2004, derived from our audited consolidated financial

statements included elsewhere in this prospectus. It also provides financial

data for, and as of the end of, the nine months ended December 31, 2005 and

2004, derived from our unaudited consolidated financial statements included

elsewhere in this prospectus. Historical results are not necessarily indicative

of the results that may be expected for any future period. When you read this

historical summary financial data, it is important that you read along with it

the historical consolidated financial statements and related notes and

"Management's Discussion and Analysis of Financial Condition and Results of

Operations" included elsewhere in this prospectus. Unless otherwise indicated

all historical financial, reserve and operations information contained in this

summary is stated in thousands.

Nine months ended

Year ended Period from Inception December 31,

March 31, (May 6, 2003) through ----------------------------------

2005 March 31, 2004 2005 2004

-------------- -------------------------- -------------- ---------------

(Unaudited) (Unaudited)

Statement of Operations Data:

Revenues $ 974 $ - $ 4,107 $ 348

Total Expenses $ 4,761 $ 787 $ 9,105 $ 2,852

Loss from Operations $ 3,788 $ 787 $ 4,999 $ 2,504

Net Loss $ 3,286 $ 614 $ 4,798 $ 2,094

Basic Loss per Share $ 0.12 $ 0.08 $ 0.15 $ 0.08

The table below sets forth a summary of our consolidated balance sheet

data as of March 31, 2005, derived from our audited consolidated financial

statements included elsewhere in this prospectus. It also provides financial

data for, and as of, the end of the nine months ended December 31, 2005, derived

from our unaudited consolidated financial statements included elsewhere in this

prospectus.

March 31, 2005 December 31, 2005

------------------ --------------------

(Unaudited)

Balance Sheet Data:

Cash and Cash Equivalents $ 9,990 $ 54,294

Inventories $ 3,227 $ 3,321

Prepaid Expenses and Other Assets, Net $ 4,172 $ 3,923

Oil and Gas Properties, Full Cost Method, Net $ 42,802 $ 54,774

Total Assets $ 61,872 $ 118,989

Total Current Liabilities $ 6,998 $ 4,031

Total Long-Term Liabilities $ 283 $ 1,141

Total Liabilities and Shareholders' Equity $ 61,872 $ 118,989

Summary Historical Reserve and Operating Data

The following table presents summary information regarding our

estimated oil and natural gas reserves as of March 31, 2005. All calculations of

estimated proved reserves have been made in accordance with the rules and

regulations of the Securities and Exchange Commission (the "SEC"), and, except

as otherwise indicated, give no effect to state income taxes. The estimates of

proved reserves are based on a reserve report prepared by Chapman Petroleum

Engineering Petroleum Ltd., ("Chapman") our independent petroleum engineers. For

additional information regarding our reserves, please read "Business and

Properties - Oil and Natural Gas Reserves" below and note 22 to our 2005 annual

consolidated financial statements.

3

Reserve Data:

Proved Reserves

As of March 31, 2005

--------------------------------------------------------------

Developed(1) Undeveloped(2) Total

----------------- -------------------- -----------------

Oil and condensate (MBbls)(3) 10,580 2,580 13,160

Natural gas (MMcf) - - -

Total BOE (MBbls) 10,580 2,580 13,160

Estimated future net revenue before income

taxes $ 182,377 $ 38,038 $ 220,415

Present value of estimated future net cash

flow before income taxes (discounted 10%

per annum)(4) $ 68,241 $ 9,037 $ 77,278

Standardized measure of discounted future

net cash flows(5) $59,354

(1) Proved developed reserves are proved reserves that are expected to be

recovered from existing wells with existing equipment and operating

methods.

(2) Proved undeveloped reserves are proved reserves which are expected to be

recovered from new wells on undrilled acreage or from existing wells where

a relatively major expenditure is required for recompletion.

(3) Includes natural gas liquids.

(4) Estimated future net reserves represents estimated future gross revenue to

be generated from the production of proved reserves, net of estimated

future production and development costs, using the average oil and gas

prices we were receiving in the Kazakhstan domestic market, as of March 31,

2005, which was $21.27 per Bbl of oil.

(5) The standardized measure of discounted future net cash flows represents the

present value of future net cash flow less the computed discount.

The following table presents summary information regarding our

historical operating data for the year ended March 31, 2005, and the period from

inception (May 6, 2003) to March 31, 2004 and for the nine months ended December

31, 2005 and 2004.

For the

Period from Nine Months Ended

For the Year Inception (May 6, December 31,

Ended 2003) to -----------------------------

March 31, 2005 March 31, 2004 2005 2004

------------------- ------------------- ------------ -------------

Production:

Oil and condensate (Bbls) 68,755 - 204,163 41,783

Natural gas liquids (Bbls) - - - -

Natural gas (Mcf) - - - -

Barrels of oil equivalent (BOE) - - - -

Average Sales Price(1)

Oil and condensate ($ per Bbl) $15.17 $ - $21.31 $13.33

Natural gas liquids ($ per Bbl) - - - -

Natural gas ($ per Mcf) - - - -

Barrels of oil equivalent ($ per BOE) - - - -

Average oil and natural gas operating

expenses including production and ad

valorem taxes ($ per BOE)(2) $ 3.08 $ - $2.64 $6.45

(1) During the period from inception through the year ended March 31, 2005, the

Company has not engaged in any hedging activities, including derivatives.

(2) Includes direct lifting costs (labor, repairs and maintenance, materials

and supplies), expensed workover costs and the administrative costs of

field production personnel, insurance and production and ad valorem taxes.

4

RISK FACTORS

Investment in our common stock involves a high degree of risk. You

should carefully consider the risks described below together with all of the

other information included in this prospectus before making an investment

decision. If any of the following risks actually occur, our business, financial

condition or results of operations could suffer. In that case, the trading price

of our common stock could decline, and you may lose all or part of your

investment.

In addition, this document may contain forward-looking statements

within the meaning of Section 27A of the Securities Act of 1933, as amended and

Section 21E of the Securities and Exchange Act of 1934, as amended.

Forward-looking statements are identified by words such as "believe,"

"anticipate," "expect," "intend," "plan," "will," "may," and other similar

expressions. In addition, any statements that refer to expectations, projections

or other characterizations of future events or circumstances are forward-looking

statements. We wish to caution readers that these forward-looking statements are

only predictions and that our business is subject to the risk factors described

below. The registrant would also like to clarify that the risk factors described

below relate to the business of BMB Munai, Inc. and its wholly-owned operating

subsidiary, Emir Oil, LLP, on a combined and consolidated basis and that no

inference should be drawn as to the magnitude of any particular risk from its

position in the list. BMB Munai, Inc. and Emir Oil, LLP, are referred to

collectively throughout this prospectus as "we," "us," "our" and "ours."

Risks Relating to the Oil and Natural Gas Industry

A substantial or extended decline in oil and natural gas prices may

adversely affect our business, financial condition, cash flow, liquidity or

results of operations and ability to meet our capital expenditure obligations

and financial commitments and implement our business strategy.

Our business is heavily dependent upon the prices of, and demand for,

oil and natural gas production and the level of such production will be subject

to wide fluctuations and depend on numerous factors beyond our control,

including the following:

o the domestic and foreign supply of oil and natural gas;

o the price and quantity of imports of crude oil and natural gas:

o political conditions and events in other oil-producing and natural

gas-producing countries, including embargoes, continued hostilities

in the Middle East, Iran, Nigeria and other sustained military

campaigns, and acts of terrorism or sabotage;

o the actions of the Organization of Petroleum Exporting Countries, or

OPEC;

o domestic government regulation, legislation and policies;

o the level of global oil and natural gas inventories;

o weather conditions;

o technological advances affecting energy consumption;

o the price availability of alternative fuels; and

o overall economic conditions.

Any continued and extended decline in the price of crude oil or natural

gas will adversely affect:

o our revenues, profitability and cash flow from operations;

o the value of our proved oil and natural gas reserves;

o the economic viability of certain of our drilling prospects;

o our borrowing capacity; and

o our ability to obtain additional capital.

5

In December 2005 we were granted our first export quota from the

Ministry of Energy and Mineral Resources of the Republic of Kazakhstan ("MEMR")

which allowed us to begin exporting oil for sale in the world market in January

2006. We have also been granted export quotas in March and April 2006. Prior to

January 2006, we were limited to selling our test production to the domestic

market in Kazakhstan. The price of oil in the domestic market in Kazakhstan is

materially lower than the price in the world market. There is no guarantee that

the Republic of Kazakhstan will continue to grant us export quotas in the

future. In the event we are not granted an export quota in the future, we will

be limited to selling our production to the domestic Kazakhstan market, which

likely will result in us realizing lower revenue per barrel of oil sold than we

would realize in the world market.

We have not entered into crude oil and natural gas price hedging

arrangements on any of our anticipated sales. However, we may in the future

enter into such arrangements in order to reduce our exposure to price risks.

Such arrangements may limit our ability to benefit from increases in oil and

natural gas prices.

Reserve estimates depend on many assumptions that may turn out to be

inaccurate. Any material inaccuracies in these reserve estimates or underlying

assumptions will materially affect the quantities and present value of our

reserves.

The process of estimating oil and natural gas reserves is complex. It

requires interpretations of available technical data and many assumptions,

including assumptions relating to economic factors. Any significant inaccuracies

in these interpretations or assumptions could materially affect the estimated

quantities and present value of reserves shown in this prospectus.

In order to prepare our estimates, we must project production rates and

timing of development expenditures. We must also analyze available geological,

geophysical, production and engineering data. The extent, quality and

reliability of this data can vary. The process also requires economic

assumptions about matters such as oil and natural gas prices, drilling and

operating expenses, capital expenditures, taxes and availability of funds.

Therefore, estimates of oil and natural gas reserves are inherently imprecise.

Actual future production, oil and natural gas prices, revenues, taxes,

development expenditures, operating expenses and quantities of recoverable oil

and natural gas reserves most likely will vary from our estimates. Any

significant variance could materially affect the estimated quantities and

present value of reserves shown in this prospectus. In addition, we may adjust

estimates of proved reserves to reflect production history, results of

exploration and development, prevailing oil and natural gas prices and other

factors, many of which are beyond our control.

You should not assume that the present value of future net revenues

from our proved reserves referred to in this prospectus is the current market

value of our estimated oil and natural gas reserves. In accordance with SEC

requirements, we generally base the estimated discounted future net cash flows

from our proved reserves on prices and costs on the date of the estimate. Actual

future prices and costs may differ materially from those used in the present

value estimate. If future values decline or costs increase, it could have a

negative impact on our ability to finance operations; individual properties

could cease being commercially viable; affecting our decision to continue

operations on producing properties or to attempt to develop properties. All of

these factors would have a negative impact on earnings and net income, and most

likely the trading price of our securities.

A substantial percentage of our proven properties are undeveloped;

therefore the risk associated with our success is greater than would be the case

if the majority of our properties were categorized as "proved developed

producing."

6

Because a substantial percentage of our proven properties are "proved

undeveloped" (approximately 20%), or "proved developed non-producing"

(approximately 65%), we will require significant additional capital to develop

such properties before they may become productive. Further, because of the

inherent uncertainties associated with drilling for oil and gas, some of these

properties may never be developed to the extent that they result in positive

cash flow. Even if we are successful in our development efforts, it could take

several years for a significant portion of our undeveloped properties to be

converted to positive cash flow.

We will be unable to produce up to 94% of our proved reserves if we are

not able to extend our current contract or obtain a new contract from the

Republic of Kazakhstan, which would likely require us to terminate our

operations.

Under our current contract for exploration of hydrocarbons on the

Aksaz, Dolinnoe and Emir fields, we have the right to produce oil and gas only

until July 2007, yet 94% of our proved reserves are scheduled to be produced

after July 2007. We have the ability to extend our current exploration contract

to July 2009. We also have the exclusive right to negotiate a commercial

production contract as per the terms of our exploration contract. If, however,

we are unable to obtain a commercial production contract prior to the expiration

of our exploration contract, we will lose our right to produce the reserves on

our current properties. If we are unable to produce those reserves, we will be

unable to realize revenues and earnings and to fund operations and we would most

likely be unable to continue as a going concern.

Prospects that we decide to drill may not yield oil or natural gas in

commercially viable quantities or quantities sufficient to meet our targeted

rate of return.

A "prospect" is a property which, based on available seismic and

geological data, we believe shows potential oil or natural gas. Our prospects

are in various stages of evaluation and interpretation. There is no way to

predict in advance of drilling and completion costs whether a prospect will be

economically viable. Even with seismic data and other technologies and the study

of producing fields in the same area, we cannot know conclusively prior to

drilling whether oil or natural gas will be present or, if present, will be

present in commercial quantities. The analysis that we perform using data from

other wells, more fully explored prospects and /or producing fields may not be

useful in predicting the characteristics and potential reserves associated with

our drilling prospects. If we drill additional unsuccessful wells, our drilling

success rate may decline and we may not achieve our targeted rate of return.

We may incur substantial losses and be subject to substantial liability

claims as a result of our oil and natural gas operations.

We are not insured against all risks. Losses and liabilities arising

from uninsured and underinsured events could materially and adversely affect our

business, financial condition or results of operations. Our oil and natural gas

exploration and production activities are subject to all of the operating risks

associated with drilling for and producing oil and natural gas, including the

possibility of:

o environmental hazards, such as uncontrollable flows of oil, natural

gas, brine, well fluids, toxic gas or other pollution into the

environment, including groundwater and shoreline contamination;

o abnormally pressured formations;

o mechanical difficulties, such as stuck oil field drilling and

service tools and casing collapse;

o fires and explosions;

o personal injuries and death; and

o natural disasters.

7

Any of these risks could adversely affect our ability to conduct

operations or result in substantial losses to our company. We may elect not to

obtain insurance if we believe that the cost of available insurance is excessive

relative to the risks presented. In addition, pollution and environmental risks

generally are not fully insurable. If a significant accident or other event

occurs that is not fully covered by insurance, it could adversely affect us.

We are subject to complex laws that can affect the cost, manner or

feasibility of doing business.

Exploration, development, production and sale of oil and natural gas

are subject to extensive federal, state, local and international regulation. We

may be required to make large expenditures to comply with governmental

regulations. Matters subject to regulation include:

o discharge permits for drilling operations;

o drilling bonds;

o reports concerning operations;

o the spacing of wells;

o unitization and pooling of properties; and

o taxation.

Under these laws, we could be liable for personal injuries, property

damage and other damages. Failure to comply with these laws may also result in

the suspension or termination of our operations and subject us to

administrative, civil and criminal penalties. Moreover, these laws could change

in ways that substantially increase our costs. Any such liabilities, penalties,

suspensions, terminations or regulatory changes could materially adversely

affect our financial condition and results of operations.

Our operations may incur substantial liabilities to comply with the

environmental laws and regulations.

Our oil and natural gas operations are subject to stringent federal,

state and local laws and regulations relating to the release or disposal of

materials into the environment or otherwise relating to environmental

protection. These laws and regulations may require the acquisition of a permit

before drilling commences, restrict the types, quantities and concentration of

substances that can be released into the environment in connection with drilling

and production activities, limit or prohibit drilling activities on certain

lands lying within wilderness, wetlands and other protected areas, and impose

substantial liabilities for pollution resulting from our operations. Failure to

comply with these laws and regulations may result in the assessment of

administrative, civil and criminal penalties, imposition of investigatory or

remedial obligations or even injunctive relief. Changes in environmental laws

and regulations occur frequently; any changes that result in more stringent or

costly waste handling, storage, transport, disposal or cleanup requirements

could require us to make significant expenditures to maintain compliance, and

may otherwise have a material adverse effect on our results of operations,

competitive position or financial condition as well as on the industry in

general. Under these environmental laws and regulations, we could be held

strictly liable for the removal or remediation of previously released materials

or property contamination regardless of whether we were responsible for the

release or whether our operations were standard in the industry at the time they

were performed.

Unless we replace our oil and natural gas reserves, our reserves and

future production will decline, which would adversely affect our cash flows and

income.

Unless we conduct successful development, exploration and exploitation

activities or acquire properties containing proved reserves, our proved reserves

will decline as those reserves are produced. Producing oil and natural gas

8

reservoirs generally are characterized by declining production rates that vary

depending upon reservoir characteristics and other factors. Our future oil and

natural gas reserves and production, and, therefore our cash flow and income,

are highly dependent on our success in efficiently developing and exploiting our

current reserves and economically finding or acquiring additional recoverable

reserves. If we are unable to develop, exploit, find or acquire additional

reserves to replace our current and future production, our cash flow and income

will decline as production declines, until our existing properties would be

incapable of sustaining commercial production.

If we do not satisfy our commitments to the government of Kazakhstan

while we are engaged in exploration and development activities we could lose our

rights to the ADE Block and the Extended Territory.

We have committed to the government of Kazakhstan to make various

capital investments and to develop the ADE Block and the Extended Territory in

accordance with specific requirements during exploration and development.

Additionally, to undertake commercial production, we will need to apply for and

be granted commercial production rights. The requirements of our current license

may be inconsistent with the terms of any new licenses we are issued.

Additionally, we may not be able to satisfy all commitments in the future. If we

fail to satisfy these commitments our contract may be cancelled. The

cancellation of our contract could have a material adverse effect on our

business, results of operations and financial condition. Although we would seek

waivers of any breaches or seek to renegotiate the terms of our commitments, we

cannot assure you that we would be successful in doing so.

Our activities, and correspondingly, our ability to generate revenue to

support operations, could be adversely affected because of inadequate

infrastructure in the region where our properties are located.

Our exploration and development activities could suffer due to

inadequate infrastructure in the region. We are working to improve the

infrastructure on our properties. Any problem or adverse change affecting our

operational infrastructure, or infrastructure provided by third parties, could

have a material adverse effect on our financial condition and results of

operations. Similarly, if we are unsuccessful in developing the infrastructure

on our properties it could have a material adverse effect on our financial

conditions and results of operations.

The unavailability or high cost of drilling rigs, equipment, supplies,

personnel and oil field services could adversely affect our ability to execute

on a timely basis our exploration and development plans within our budget.

Shortages or the high cost of drilling rigs, equipment, supplies or

personnel could delay or adversely affect our development and exploration

operations. As the price of oil and natural gas increases, the demand for

production equipment and personnel will likely also increase, potentially

resulting, at least in the near-term, in shortages of equipment and personnel.

In addition, larger producers may be able to secure access to such equipment by

offering drilling companies more lucrative terms. If we are unable to acquire

access to such resources, or can obtain access only at higher prices, not only

would this potentially delay our ability to convert our reserves into cash flow,

but this could also significantly increase the cost of producing those reserves,

thereby having a negative impact on anticipated net income.

The unavailability or high price of transportation systems could

adversely affect our ability to deliver our production to oil and natural gas

markets on terms that would allow us to operate profitably, or at all.

Because of the location of our properties, the crude oil we produce

must be transported by truck or by rail. In the future it will likely also be

transported by pipelines. These railways and pipelines are operated by

9

state-owned entities or other third parties, and there can be no assurance that

these transportation systems will always be functioning and available, or that

the transportation costs will remain at acceptable levels. In addition, any

increase in the cost of transportation or reduction in its availability to us

could have a material adverse effect on our results of operations. There is no

assurance that we will be able to procure sufficient transportation capacity on

economical terms, if at all.

Competition in the oil and natural gas industry is intense, which may

adversely affect our ability to compete.

We operate in a highly competitive environment for acquiring properties,

marketing oil and natural gas and securing trained personnel. Many of our

competitors possess and employ financial, technical and personnel resources

which are substantially greater than ours, this can be particularly important in

the areas in which we operate. Those companies may be able both to pay more for

productive oil and natural gas properties and exploratory prospects and to

evaluate, bid for and purchase a greater number of properties and prospects than

our financial or personnel resources permit. Our ability to acquire additional

prospects and to find and develop reserves in the future will depend on our

ability to evaluate and select suitable properties and to consummate

transactions in a highly competitive environment. There is substantial

competition for capital available for investment in the oil and natural gas

industry. We may not be able to compete successfully in the future in acquiring

prospective reserves, developing reserves, marketing hydrocarbons, attracting

and retaining quality personnel or raising additional capital.

Risks Relating to Our Business

The loss of senior management and key personnel could adversely affect

us.

Our success is dependent on the performance of our senior management

and key technical personnel each of whom has extensive experience in the oil and

gas industry. The loss of such individuals, in particular, Boris Cherdabayev,

our CEO and Chairman of our Board of Directors, or Toluesh Tolmakov, the General

Director of Emir Oil, our wholly-owned subsidiary, could have an adverse effect

on our business. We do not have employment agreements in place with our senior

management or key employees. We do not currently carry key man insurance for any

of our senior management or key employees, nor do we anticipate obtaining key

man insurance in the foreseeable future.

If you purchase shares of our stock, your investment will be subject to

the same risks inherent in international operations, including, but not limited

to, adverse governmental actions, political risks, and expropriation of assets,

loss of revenues and the risk of civil unrest or war.

We believe that the present policies of the government of the Republic

of Kazakhstan are favorable to foreign investment and to exploration and

production and we are not aware of any impending changes. While there is a

certain amount of bureaucratic "red tape" we have significant experience working

in Kazakhstan, and good relationships with government agencies at many levels.

We, however, remain subject to all the risks inherent in international

operations, including adverse governmental actions, uncertain legal and

political systems, and expropriation of assets, loss of revenues and the risk of

civil unrest or war. Our primary oil and gas properties are located in

Kazakhstan, which until 1990 was part of the Soviet Union. Kazakhstan retains

many of the laws and customs of the former Soviet Union, but has and is

continuing to develop its own legal, regulatory and financial systems. As the

political and regulatory environment changes, we may face uncertainty about the

interpretation of our agreements; in the event of dispute, we may have limited

recourse within the legal and political system.

10

If we are successful in establishing commercially producible reserves

on our properties, an application will be made for a commercial production

contract. We have the exclusive right to negotiate this contract for the ADE

Block and Extended Territory, and the government is required to conduct these

negotiations under the "Law of Petroleum." Such contracts are customarily

awarded upon determination that the field is capable of commercial rates of

production and that we have complied with the other terms of our license and

exploration contract. The terms of the commercial production contract will

establish the royalty and other payments due to the government in connection

with commercial production. At the time the commercial production contract is

issued, we will be required to begin repaying the government its historical

investment costs of exploration and development of the ADE Block and the

Extended Territory. Our obligation associated with the ADE Block is

approximately $6 million. Our obligation associated with the Extended Territory

has not yet been determined and is currently being negotiated. If satisfactory

terms for commercial production rights cannot be negotiated, it could have a

material adverse effect on our financial position.

Risks Relating to an Investment in Our Securities

You may have difficulty reselling the shares you acquire in this

offering because of the limited trading volume of your common stock.

Our stock has limited trading volume on the Over-the-Counter Bulletin

Board and is not listed on a national exchange. Moreover, a significant

percentage of our outstanding common stock is "restricted" and therefore subject

to the resale restrictions set forth in Rule 144 of the rules and regulations

promulgated by the Securities and Exchange Commission under the Securities Act

of 1933. These factors could adversely affect the liquidity, trading volume,

price and transferability of our common shares.

There are a large number of shares that may be sold in the market as a

result of this offering, which may cause the price of our common stock to

decline.

As of May 12, 2006, 43,245,657 shares of our common stock were

outstanding. We are registering 13,846,427 shares of our common stock, pursuant

to this prospectus, all of which are already outstanding. Any person acquiring

shares of common stock covered by this registration statement, from any party

other than an "affiliates," will acquire freely tradable shares without

restriction or further registration under federal securities laws. Sales of a

substantial number of shares of our common stock in the public markets, or the

perception that these sales may occur, could cause the market price of our

common stock to decline and could materially impair our ability to raise capital

through the sale of additional equity securities or to enter into strategic

acquisitions with third parties.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements that are subject to a

number of risks and uncertainties, many of which are beyond our control, and may

include statements about our:

o business strategy;

o reserves;

o financial strategy;

o production;

o uncertainty regarding our future operating results;

o plans, objectives, expectations and intentions that are not

historical.

All statements, other than statements of historical fact included in

this prospectus, regarding our strategy, future operations, financial position,

estimated revenues and losses, projected costs, prospects, plans and objectives

of management are forward-looking statements. When used in this prospectus, the

11

words "could," "believe," "anticipate," "intend," "estimate," "expect,"

"project" and similar expressions are intended to identify forward-looking

statements, although not all forward-looking statements contain such identifying

words. All forward-looking statements speak only as of the date of this

prospectus. You should not place undue reliance on these forward-looking

statements. Although we believe that our plans, intentions and expectations

reflected in or suggested by the forward-looking statements we make in this

prospectus are reasonable, we can give no assurance that these plans, intentions

or expectations will be achieved. We disclose important factors that could cause

our actual results to differ materially from our expectations under "Risk

Factors," "Management's Discussion and Analysis of Financial Condition and

Results of Operations" and elsewhere in this prospectus. These cautionary

statements qualify all forward-looking statements attributable to us or persons

acting on our behalf.

USE OF PROCEEDS

The selling stockholders will receive all of the net proceeds from the

sale of our common stock offered by this prospectus. Accordingly, we will not

receive any proceeds from the sale of the common stock.

SELLING SECURITY HOLDERS

The following table provides information regarding the beneficial

ownership of the outstanding shares of our common stock by the selling

stockholders. Except as may be identified in the footnotes to the table, none of

the selling security holders has held any position, office or otherwise had a

material relationship with BMB or any of its predecessors or affiliates in the

past three years. Percentage of beneficial ownership after the offering is based

on 43,245,657 shares of our common stock outstanding as of May 12, 2006. The

selling stockholders may offer the shares for sale from time to time in whole or

in part. Except where otherwise noted, the selling stockholders named in the

following table have, to our knowledge, sole voting and investment power with

respect to the shares beneficially owned by them.

Beneficial Ownership Beneficial Ownership

Before Offering After Offering(2)

Name Shares % Shares Offered(1) Shares %

- -------------------------------------- ---------- ------ ----------------- --------- ------

DKR Saturn Event Driven Holding Fund

LTD(3) 1,079,953 2.5% 1,079,953 0 *

Front Street Investment Management,

Inc. (4) 62,500 * 62,500 0 *

Douglas M. Lane 15,000 * 15,000 0 *

Credifinance Capital Corp. (5) 452,083 1.0% 452,083 0 *

Firebird Global Master Fund,

Ltd. (6) 88,000 * 88,000 0 *

Bear Stearns FBO Firebird Global

Master Fund, Ltd. (6) 150,000 * 100,000 50,000 *

Vertex One Asset Management, Inc. (7) 300,000 * 300,000 0 *

Firebird Republics Fund, Ltd. (8) 533,333 1.2% 533,333 0 *

William McGee 103,367 * 93,367 10,000 *

Douglas Francis Roche 7,060 * 7,060 0 *

Bradley Peech 12,500 * 12,500 0 *

Stanley Smith 45,078 * 15,176 29,902 *

WTC-CIF Energy Portfolio (nominee:

Finwell & Co.) (9) 23,000 * 15,000 8,000 *

WTC-CIF Energy Portfolio (nominee:

Landwave & Co.) (10) 163,000 * 114,000 49,000 *

Spindrift Partners, L.P. (11) 247,000 * 141,000 106,000 *

Spindrift Investors (Bermuda) L.P. (12) 317,000 * 161,000 156,000 *

Aton International Ltd.(13) 1,226,121 2.8% 1,226,121 0 *

12

Roytor & Co. (14) 200,000 * 200,000 0 *

Roytor & Co. (15) 200,000 * 200,000 0 *

Anthony Richard Brocas Burrows 4,500 * 4,500 0 *

Brewin Nominees (Channel Islands)

Ltd.(16) 1,760 * 1,760 0 *

Brewin Nominees Ltd. (17) 1,400 * 1,400 0 *

Giltspur Nominees Ltd.(18) 58,990 * 58,990 0 *

Genesis Smaller Companies SICAV

(Nominee: JPMorgan Chase Bank NY)(19) 227,000 * 227,000 0 *

Genesis Emerging Markets

Opportunities Fund Ltd. (20) 1,098,000 2.5% 1,098,000 0 *

Global Undervalued Securities Master

Fund(21) 200,000 * 200,000 0 *

Drake Associates, L.P. (22) 70,000 * 70,000 0 *

Firebird Avrora Fund, Ltd. (8) 626,190 1.4% 533,333 92,857 *

Firebird New Russia Fund, Ltd. (8) 125,334 * 125,334 0 *

Touradji Global Resources Master

Fund, Ltd. (23) 2,259,265 5.2% 1,250,000 1,009,265 2.3%

QVT Fund LP(24) 250,000 * 250,000 0 *

TCW Americas Development

Association, L.P.(25) 330,000 * 330,000 0 *

S.A.C. Capital Associates, LLC(26) 300,000 * 300,000 0 *

Invesco Taiga(27) 55,327 * 55,327 0 *

Eastern Europe and Russian Mother

Equity Fund(28) 276,632 * 276,632 0 *

State Street Emerging Markets (210)(29) 177,400 * 177,400 0 *

AGF Marches Emergents (260) (29) 50,300 * 50,300 0 *

State Street Active Asie (360) (29) 69,900 * 69,900 0 *

Disclaim & Co. (2D09) (29) 437,800 1.0% 437,800 0 *

Olynthus & Co. (9T02) (29) 133,900 * 133,900 0 *

Headguard & Co. (ZV93) (29) 106,600 * 106,600 0 *

Portbird & Co. (N42N) (29) 47,600 * 47,600 0 *

Mildbreeze & Co. (DA50) (29) 40,700 * 40,700 0 *

Squab & Co. (DU2M) (29) 35,800 * 35,800 0 *

Cudd & Co. Nominee for JP Morgan

Chase Bank(30) 133,800 * 133,800 0 *

Cudd & Co. Nominee for JP Morgan

Chase Bank(31) 78,500 * 78,500 0 *

Cudd & Co. Nominee for JP Morgan

Chase Bank(32) 399,200 * 399,200 0 *

Cudd & Co. Nominee for JP Morgan

Chase Bank(33) 174,300 * 174,300 0 *

MTBJ JPM Russia & Eastern Europe

Fund(34) 566,300 1.3% 566,300 0 *

Cudd & Co. Nominee for JP Morgan

Chase Bank(35) 1,740,600 4.0% 1,740,600 0 *

Gerlach & Co., Citibank NA IC&D(36)

55,358 * 55,358 0 *

* Less than 1%.

(1) Represents the number of shares we are required to register pursuant to the

registration rights of the selling stockholders.

(2) Assumes all shares being offered under this prospectus will be sold by the

selling stockholders.

13

(3) DKR Saturn Event Driven Holding Fund, LTD. has informed us that Ron

Phillips has dispositive and voting power for all of its shares in our

Company.

(4) Front Street Investment Management, Inc. has informed us that Frank Mersch

has dispositive and voting power for all of its shares in our Company.

(5) Cedifinance Capital Corp. has informed us that Georges Benarroch has

dispositive and voting power for all of its shares in our Company. Mr.

Benarroch currently serves on our board of directors and is the former CEO

of our predecessor company.

(6) Firebird Global Master Fund, Ltd. has informed us that James Passin has

dispositive and voting power for all of its shares in our Company.

(7) Vertex One Asset Management, Inc. has informed us that John Thiessen has

dispositive and voting power for all of its shares in our Company.

(8) Firebird Republics Fund, Ltd., Firebird Avrora Fund, Ltd., and Firebird New

Russia Fund, Ltd., have each informed us that Harvey Sawikin and Ian Hague

have dispositive and voting power for all of our shares held by each of

these funds.

(9) Wellington Management Company, LLP ("Wellington") is an investment adviser

registered under the Investment Advisers Act of 1940, as amended.

Wellington, in such capacity is deemed to share beneficial ownership of the

shares held by WTC-CIF Energy Portfolio (nominee: Finwell & Co.).

(10) Wellington Management Company, LLP ("Wellington") is an investment adviser

registered under the Investment Advisers Act of 1940, as amended.

Wellington, in such capacity is deemed to share beneficial ownership of the

shares held by WTC-CIF Energy Portfolio (nominee: Landwave & Co.).

(11) Wellington Management Company, LLP ("Wellington") is an investment adviser

registered under the Investment Advisers Act of 1940, as amended.

Wellington, in such capacity is deemed to share beneficial ownership of the

shares held by Spindrift Partners, L.P.

(12) Wellington Management Company, LLP ("Wellington") is an investment adviser

registered under the Investment Advisers Act of 1940, as amended.

Wellington, in such capacity is deemed to share beneficial ownership of the

shares held by Spindrift Investors (Bermuda) L.P.

(13) Aton International Ltd., has informed us that Charalambos Michaelides has

dispositive and voting power for all of its shares in our Company.

(14) Roytor & Co. holds these shares for the benefit of RAB Special Situations

(Master) Fund Limited. RAB Special Situations (Master) Fund Limited has

informed us that Mr. W.P.S. Richards has dispositive and voting power for

all of its shares in our Company.

(15) Roytor & Co. holds these shares for the benefit of RAB Energy Fund Ltd. RAB

Energy Fund Ltd. has informed us that Gavin Wilson has dispositive and

voting power for all of its shares in our Company.

(16) Brewin Nominess (Channel Islands) Ltd. has informed us that Obelisk Trust

Ltd., Guernsey, has dispositive and voting power for all of its shares in

our Company.

(17) Brewin Nominees Ltd. has informed us that Brewin Dolphin Senior Staff

Pension Scheme has dispositive and voting power for all of its shares in

our Company.

(18) Giltspur Nominess Ltd. has informed us that it holds these shares for the

benefit of the following persons or entities, each of whom has the

dispositive and voting power over the shares of our Company each

respectively owns: Mr. R C M Westrup - 2,400 shares; Gabriel Mackintosh -

2,200 shares; Anthony Mackintosh - 7,400 shares; Mrs. V R MacAndrew - 2,200

shares; Mr. A B Greene - 3,700 shares; Mr. A Bridgewater - 2,200 shares;

Mr. R J Coverley - 1,500 shares; Mr. D J Clark - 2,000 shares; Mr. J K

Rylands - 5,440 shares; Mr. J S Bickersteth - 1,500 shares; Mrs.

Tarrant-Smith - 1,500 shares; Mr. D B E Pike - 2,700 shares; Duet

Investements Ltd., Monaco - 10,750 shares; and Pension Scheme of E Lebas

Ltd. - 13,500 shares.

(19) Genesis Fund Managers, LLP ("GFM") is an investment adviser registered

under the Investment Advisers Act of 1940, as amended. GFM, in such

capacity is deemed to have dispositive and voting power for all of the

shares held by Genesis Smaller Companies SICAV (Nominee: JPMorgan Chase

Bank NY.)

(20) Genesis Asset Managers, LLP ("GAM") is an investment adviser registered

under the Investment Advisers Act of 1940, as amended. GAM, in such

capacity is deemed to have dispositive and voting power for all of the

shares held by Genesis Emerging Markets Opportunities Fund Ltd.

(21) Kleinheinz Capital Partners, Inc. ("Kleinheinz") is an investment adviser

registered under the Investment Adviser Act of 1940, as amended.

Kleinheinz, in such capacity, is deemed to have dispositive and voting

power for all of the shares held by Global Undervalued Securities Master

Fund.

(22) Drake Associates, L.P. has informed us that Alec Rutherfurd has dispositive

and voting power for all of its shares in our Company.

(23) Touradji Global Resources Master Funds, Ltd., has informed us that Paul

Touradji has dispositive and voting power for all of its shares in our

Company.

14

(24) QVT Fund LP has informed us that its general manager, QVT Associates GP LLC

and its investment manager QVT Financial LP each have dispositive and

voting power over all of its shares in our Company.

(25) TCW Americas Development Association, L.P. has informed us that Penelope

Foley and David I. Robbins have dispositive and voting power for all of its

shares in our Company.

(26) S.A.C. Capital Associates, LLC, has informed us that pursuant to investment

agreements, each of S.A.C. Capital Advisors, LLC, a Delaware limited

liability company ("SAC Capital Advisors") and S.A.C. Capital Management,

LLC, a Delaware limited liability company ("SAC Capital Management") share

dispositive and voting power with respect to the shares held by S.A.C.

Capital Associates, LLC. Mr. Steven Cohen controls both SAC Capital

Advisors and SAC Capital Management. Each of SAC Capital Advisors, SAC

Capital Management and Mr. Cohen disclaim beneficial ownership of any of

the securities held by S.A.C. Capital Associates, LLC.

(27) Invesco Taiga has informed us that Peter Jarvis, the fund manager of

Invesco Asset Management, has dispositive and voting power for all of its

shares in our Company.

(28) Eastern Europe & Russian Equity Mother Fund has informed us that Peter

Jarvis, the fund manager of Invesco Asset Management, has dispositive and

voting power for all its shares in our Company.

(29) Each of State Street Emergents (210), AGF Marches Emergents (260), State

Street Active Asie (360), Disclaim & Co. (2D09), Olynthus & Co. (9T02),

Headguard & Co. (ZV93), Portbird & Co. (N42N), Mildbreeze & Co. (DA50) and

Squab & Co. (DU2M) has informed us that State Street Global Advisors, a

division of State Street Bank & Trust Company may be deemed the beneficial

owner of the shares held by each account because State Street Global

Advisors has dispositive power for all shares of our Company held by each

account.

(30) JP Morgan Chase Bank holds these shares for the benefit of OP Eastern

European Fund (the "Eastern European Fund"). We have been informed that

JPMAM (UK) Ltd. ("JPMAM"), an investment adviser registered under the

Investment Advisers Act of 1940, as amended, acts as the investment adviser

to Eastern European Fund. In its capacity as investment adviser to Eastern

European Fund, JPMAM may be deemed to have voting and dispositive control

over the shares held for the benefit of Eastern European Fund.

(31) JP Morgan Chase Bank holds these shares for the benefit of JPM New Europe

Fund ("New European Fund"). We have been informed that JPMAM (UK) Ltd.

("JPMAM"), an investment adviser registered under the Investment Advisers

Act of 1940, as amended, acts as the investment adviser to New Europe Fund.

In its capacity as investment adviser to New Europe Fund, JPMAM may be

deemed to have voting and dispositive control over the shares held for the

benefit of New Europe Fund.

(32) JP Morgan Chase Bank holds these shares for the benefit of JPM Emerging

Europe Equity Fund ("Emerging Europe"). We have been informed that JPMAM

(UK) Ltd. ("JPMAM"), an investment adviser registered under the Investment

Advisers Act of 1940, as amended, acts as the investment adviser to

Emerging Europe. In its capacity as investment adviser to Emerging Europe,

JPMAM may be deemed to have voting and dispositive control over the shares

held for the benefit of Emerging Europe.

(33) JP Morgan Chase Bank holds these shares for the benefit of JPM Russia Fund

("Russia Fund"). We have been informed that JPMAM (UK) Ltd. ("JPMAM"), an

investment adviser registered under the Investment Advisers Act of 1940, as

amended, acts as the investment adviser to Russia Fund. In its capacity as

investment adviser to Russia Fund, JPMAM may be deemed to have voting and

dispositive control over the shares held for the benefit of Russia Fund.

(34) MTBJ JPM Russian and Eastern Europe Fund has informed us that JPMAM (UK)

Ltd. ("JPMAM"), an investment adviser registered under the Investment

Advisors Act of 1940, as amended, acts as the investment adviser to MTBJ

JPM Russian and Eastern Europe Fund. In its capacity as investment adviser

to MTBJ JPM Russian and Eastern Europe Fund, JPMAM may be deemed to have

voting and dispositive control over the shares held for the benefit of MTBJ

JPM Russian and Eastern Europe Fund.

(35) JP Morgan Chase Bank holds these shares for the benefit of JPM Eastern

Europe Equity Fund ("Eastern Europe"). We have been informed that JPMAM

(UK) Ltd. ("JPMAM"), an investment adviser registered under the Investment

Advisers Act of 1940, as amended, acts as the investment adviser to Eastern

Europe. In its capacity as investment adviser to Eastern Europe, JPMAM may

be deemed to have voting and dispositive control over the shares held for

the benefit of Eastern Europe.

(36) Gerlach & Co., Citibank NA IC&D holds these shares for the benefit of

Baring Asset Management New Russia Fund ("Baring"). Baring has informed us

that Edward Remington Hobbs has dispositive and voting power for all of its

shares in our Company.

15

PLAN OF DISTRIBUTION

The selling stockholders ,which as used herein includes donees,

pledges, transfers or other successors-in-interest selling shares of common

stock or interests in shares of common stock received after the date of this

prospectus from a selling stockholder as a gift, pledge, partnership

distribution or other transfer, may, from time to time, sell, transfer or

otherwise dispose of any or all their shares of common stock or interests in

shares of common stock on any stock exchange, market or trading facility on

which the shares are traded or in private transactions. These dispositions may

be at fixed prices, at prevailing market prices at the time of sale, at prices

related to the prevailing market price, at varying prices determined at the time

of sale, or at negotiated prices.

The selling stockholders may use any one or more of the following

methods when disposing of shares or interests therein:

o ordinary brokerage transactions and transactions in which the

broker-dealer solicits purchases;

o block trades in which the broker-dealer will attempt to sell the

shares as agent, but may position and resell a portion of the block

as principal to facilitate the transaction;

o purchases by a broker-dealer as principal and resale by the

broker-dealer for its account;

o an exchange distribution in accordance with the rules of the

applicable exchange;

o privately negotiated transactions;

o short sales effected after the date of this prospectus;

o the writing or settlement of options or other hedging transactions,

whether through an options exchange or otherwise;

o agreements with broker-dealers to sell a specified number of such

shares at a stipulated price per share;

o a combination of any such methods of sale; and

o any other method permitted pursuant to applicable law.

The selling stockholders may, from time to time, pledge or grant a

security interest in some or all of the shares of common stock owned by them; if

they default in the performance of their secured obligations, the pledges or

secured parties may offer and sell the shares of common stock, from time to

time, under this prospectus, or under an amendment to this prospectus under Rule

424(b) (3) or other applicable provision of the Securities Act of 1933 amending

the list of selling stockholders to include the pledge, transferee or other

successors in interest as selling stockholders under this prospectus. The

selling stockholders may also transfer the shares of common stock in other

circumstances, in which case the transferees, pledges or other successors in

interest will be the selling beneficial owners for purposes of this prospectus.

In connection with the sale of our common stock or interests therein,

the selling stockholders may enter into hedging transactions with broker-dealers

or other financial institutions, who may in turn engage in short sales of the

common stock in the course of hedging the positions they assume. The selling

stockholders may also sell shares of our common stock short and deliver these

securities to close out their positions, or loan or pledge the common stock to

broker-dealers who in turn may sell these securities. The selling stockholders

may also enter into option or other transactions with broker-dealers or other

financial institutions which could result in the creation of one or more

derivative securities requiring delivery to such broker-dealer or other

financial institution of shares offered by this prospectus, such broker-dealer

or other financial institution may resell these shares pursuant to this

prospectus (as supplemented or amended to reflect such transaction).

The aggregate proceeds to the selling stockholders from the sale of the

common stock offered by them will be the purchase price of the common stock less

discounts or commissions, if any. Each of the selling stockholders reserves the

right to accept and, together with their agents from time to time, to reject, in

whole or in part, any proposed purchase of common stock to be made directly or

through agents. We will not receive any of the proceeds from this offering.

16

The selling stockholders may also resell all or a portion of the shares

in open market transactions in reliance upon Rule 144 under the Securities Act

of 1933, provided that they meet the criteria and conform to the requirements of

that rule.

The selling stockholders and any underwriters, broker-dealers or agents

that participate in the sale of the common stock or interests therein may be

"underwriters" within the meaning of Section 2(11) of the Securities Act. Any

discounts, commissions, concessions or profit they earn on any resale of the

shares may be underwriting discounts and commissions under the Securities Act.

Discounts, concessions, commissions and similar selling expenses, if

any, that can be attributed to the sale of the securities will be paid by the

selling stockholders and /or the purchasers. Each selling stockholder has

represented and warranted to us that it acquired the securities which are

subject to this registration statement in the ordinary course of such selling

stockholder's business and, at the time of its purchase of such securities such

selling stockholders had no agreements or understandings, directly or indirectly

,with any person to distribute any such securities. We have advised each selling

stockholder that it may not use shares registered under this registration

statement to cover short sales of common stock made prior to the date on which

registration statement shall have been declared effective by the SEC. Selling

stockholders who are "underwriters" within the meaning of Section 2(11) of the

Securities Act of 1933 will be subject to the prospectus delivery requirements

of the Securities Act of 1933.

To the extent required, the shares of our common stock to be sold, the

names of the selling stockholders, the respective purchase prices and public

offering prices, the names of any agents, dealers or underwriters, the amount of

any applicable commissions or discounts with respect to a particular offer will

be set forth in an accompanying prospectus supplement or, if appropriate, a

post-effective amendment to the registration statement that includes this

prospectus.

In order to comply with the securities laws of some states, if

applicable, the common stock may be sold in these jurisdictions only through

registered or licensed brokers or dealers. In addition, in some sates the common

stock may not be sold unless it has been registered or qualified for sale or an

exemption from registration or qualification requirements is available and

complied with.

We have advised the selling stockholders that the anti-manipulation

rules of Regulation M under the Securities Exchange Act of 1934 may apply to

sales of shares in the market and to the activities of the selling stockholders

and their affiliates.

We have agreed to indemnify the selling stockholders against

liabilities, including liabilities under the Securities Act of 1933 and state

securities laws, relating to the registration of the shares offered by this

prospectus. In addition, we will make copies of this prospectus (as it may be

supplemented or amended from time to time) available to the selling stockholders

who may indemnify any broker-dealer that participates in transactions involving

the sale of the shares against certain liabilities, including liabilities

arising under the Securities Act of 1933.

We have agreed with the selling stockholder to keep the registration

statement of which this prospectus constitutes a part effective until the

earlier (1) such time as all of the shares covered by this prospectus have been

disposed of pursuant to and in accordance with the registration statement or (2)

the date on which the shares may be sold pursuant to Rule 144(k) of the

Securities Act of 1933.

LEGAL PROCEEDINGS

In December 2003, a complaint was filed in the 15th Judicial Court in

and for Palm Beach County, Florida, naming, among others, us, Georges Benarroch

and Alexandre Agaian, current or former BMB directors, as defendants. The

17

plaintiffs, Brian Savage, Thomas Sinclair and Sokol Holdings, Inc., allege

claims of breach of contract, unjust enrichment, breach of fiduciary duty,

conversion and violation of a Florida trade secret statute in connection with a

business plan for the development Aksaz, Dolinnoe and Emir oil and gas fields

owned by Emir Oil, LLP. The parties mutually agreed to dismiss this lawsuit

without prejudice.

In April 2005, Sokol Holdings also filed a complaint in United States

District Court, Southern District of New York alleging that BMB Munai, Inc.,

Boris Cherdabayev, Alexandre Agaian, Bakhytbek Baiseitov, Mirgali Kunayev and

Georges Benarroch wrongfully induced Toleush Tolmakov to breach a contract under

which Mr. Tolmakov had agreed to sell to Sokol Holdings 70% of his 90% interest

in Emir Oil LLP.

In October 2005, Sokol Holdings amended its complaint in the U.S.

District Court in New York to add Brian Savage and Thomas Sinclair as plaintiffs

and to add Credifinance Capital, Inc., and Credifinance Securities, Ltd.,

(collectively "Credifinance") as defendants in the matter. The amended complaint

alleges tortious interference with contract, specific performance, breach of

contract, unjust enrichment, breach of fiduciary duty by Georges Benarroch,

Alexandre Agaian and Credifinance, conversion, breach of fiduciary duty by Boris

Cherdabayev, Mirgali Kunayev and Bakhytbek Baisietov, misappropriation of trade

secrets, tortious interference with fiduciary duty by Mr. Agaian, Mr. Benarroch

and Credifinance and aiding and abetting breach of fiduciary duty by Mr.

Benarroch, Mr. Agaian and Credifinance in connection with a business plan for

the development of the Aksaz, Dolinnoe and Emir oil and gas fields owned by Emir

Oil, LLP. The plaintiffs have not named Toluesh Tolmakov as defendant in the

action nor have the plaintiffs ever brought claims against Mr. Tolmakov to

establish the existence or breach of any legally binding agreement between the

plaintiffs and Mr. Tolmakov. The plaintiffs seek damages in an amount to be

determined at trial, punitive damages, specific performance and such other

relief as the Court finds just and reasonable.

We have retained the law firm of Bracewell & Giuliani LLP in New York,

New York to represent us in the lawsuit. We moved for dismissal of the amended

complaint or for a stay pending arbitration in Kazakhstan. That motion was

denied, without prejudice to refiling it, to enable defendants to produce

documents to plaintiffs relating to the issues raised in the motion. The motion

will be refiled after the completion of the document production.

In the opinion of management, the resolution of this lawsuit will not

have a material adverse effect on our financial condition, results of operations

or cash flows.

In November 2005, we learned that the Company had been added as a

defendant in a lawsuit filed by Bank CenterCredit against Optima Systems, LLP,

KazOvoshProm Company, LLP and Intexi LLP and a number of other parties. The

lawsuit was filed in the Special Interregional Economic Court of Almaty,

Kazakhstan. Under Kazakh law, it is illegal for a party to purchase stock of a

bank with borrowed funds. The lawsuit alleges that Optima Systems, KazOvoshProm

Company and Intexi illegally purchased shares of Bank CenterCredit in open

market transactions in the Kazakhstan Stock Market from a number of parties,

including BMB Munai, with borrowed funds.

Bank CenterCredit has delivered a letter to us confirming that we have

been joined in this matter to comply with the procedural requirements of Kazakh

law and acknowledging our Company acted as a party to the transaction as a good

faith seller of shares of the Bank. The Bank further acknowledges that the case

has no property or material nature as it relates to BMB Munai. The Bank also

guarantees to reimburse us for any expenses we may incur in connection with the

litigation.

In the opinion of management, the resolution of this lawsuit will not

have a material adverse effect on our financial condition, results of operations

or cash flows.

18

Other than the foregoing, to the knowledge of management, there is no

other material litigation or governmental agency proceeding pending or

threatened against the Company or our management.

DIRECTORS, EXECUTIVE OFFICERS, PROMOTERS AND

CONTROL PERSONS

The following table sets forth our directors, executive officers,

promoters and control persons, their ages, and all offices and positions held

within the Company. Directors are elected for staggered terms ranging from a

period of one to three years and thereafter they serve until their successor is

duly elected by the stockholders and qualified. Officers and other employees

serve at the will of the Board of Directors.

Name Age Positions with BMB Director Since

- ---- --- ------------------ --------------

Boris Cherdabayev 51 Chairman of the Board of Directors November 2003

and Chief Executive Officer

Georges Benarroch 57 Director November 2003

Sanat Kasymov 30 Chief Financial Officer

Adam Cook 32 Secretary

Troy Nilson 40 Director December 2004

Stephen Smoot 50 Director January 2005

Askar Tashtitov 26 President

Valery Tolkachev 37 Director December 2003

The above individuals will serve as our officers and/or directors. A

brief description of their background and business experience follows:

Boris Cherdabayev. Mr. Cherdabayev joined BMB Holding, Inc., and

assumed his current positions in May 2003. From May 2000 to May 2003, Mr.

Cherdabayev served as Director at TengizChevroil, LLP a multination oil and gas

company owned by Chevron, ExxonMobil, KazMunayGas and LukOil. From 1998 to May

2000, Mr. Cherdabayev served as a member of the Board of Directors,

Vice-President of Exploration and Production and Executive Director on Services

Projects Development for NOC "Kazakhoil", an oil and gas exploration and

production company. From 1983 to 1988, he served as a people's representative at

Novouzen City Council (Kazakhstan) and from 1994 to 1998; he served as a

people's representative at Mangistau Oblast Maslikhat (regional level

legislative structure) and a Chairman of the Committee on Law and Order. For his

achievements Mr. Cherdabayev has been awarded with a national "Kurmet" order.

Mr. Cherdabayev earned an engineering degree from the Ufa Oil & Gas Institute,

with a specialization in "machinery and equipment of oil and gas fields" in

1976. Mr. Cherdabayev also earned an engineering degree from Kazakh Polytechnic

Institute, with a specialization in "mining engineer on oil and gas fields'

development." During his career he also completed an English language program in

the USA, the NIAI-D Program (Chevron Advanced Management Program) at Chevron

Corporation offices in San-Francisco, CA, USA, and the CSEP Program (Columbia

Senior Executive Program) at Columbia University, New York, NY USA. Mr.

Cherdabayev is not a director or nominee of any reporting company.

Georges Benarroch. Mr. Benarroch has been a member of the Investment

Dealer Association of Canada and has served as the president and chief executive

officer of Euro Canadian Securities Limited and its successor company,

Credifinance Securities Limited, an institutional investment bank, based in

Toronto, a member of the Toronto Stock Exchange and the Montreal Exchange since

1982. Credifinance Securities Limited has been one of the North American

pioneers in providing investment banking and equity research coverage of

companies in the Former Soviet Union ("FSU.") Since 1994, Credifinance

Securities Limited has acted as agent and/or underwriter, stock exchange